Coriander Market Update: Stable Prices Amid Tight Supply and Weak Exports

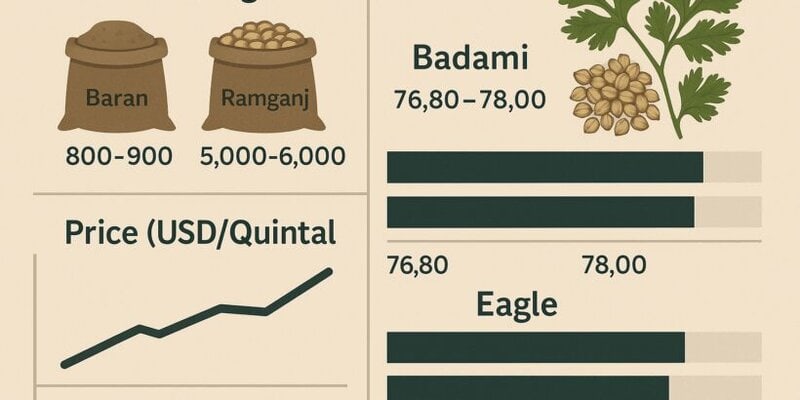

The coriander market in India, particularly in Rajasthan's major trading hubs, is currently navigating a period of remarkable stability despite a backdrop of tightening supply and subdued export demand. Daily arrivals in key mandis such as Ramganj and Baran have seen a sharp drop, with volumes in Ramganj at 5,000–6,000 bags and Baran at just 800–900 bags, reflecting farmers' reluctance to sell at prices below their expectations. This supply-side restraint comes after earlier disruptions caused by heavy wheat arrivals, which delayed coriander auctions and further tightened the market. Although prices dipped earlier this month by about USD 2.40–3.60 per quintal, a modest recovery is now visible, with premium varieties like Eagle and Badami stabilizing in both Ramganj and Baran.

Despite the recent stability, the broader picture is less optimistic. Export data from the Spices Board highlights a dramatic fall in both volume and value for the 2024–25 season compared to last year, reflecting weaker global demand and possibly increased competition from other origins. On the production front, Gujarat has recorded a marginal increase in sowing, but Rajasthan and Madhya Pradesh—key coriander-producing states—have seen a significant 25% reduction in acreage due to adverse weather and farmer sentiment. With the market currently balanced between limited arrivals and restrained demand, coriander prices are expected to remain range-bound in the near term, though weather risks and export trends warrant close monitoring.

Despite the recent stability, the broader picture is less optimistic. Export data from the Spices Board highlights a dramatic fall in both volume and value for the 2024–25 season compared to last year, reflecting weaker global demand and possibly increased competition from other origins. On the production front, Gujarat has recorded a marginal increase in sowing, but Rajasthan and Madhya Pradesh—key coriander-producing states—have seen a significant 25% reduction in acreage due to adverse weather and farmer sentiment. With the market currently balanced between limited arrivals and restrained demand, coriander prices are expected to remain range-bound in the near term, though weather risks and export trends warrant close monitoring.

📈 Prices

🌍 Supply & Demand

- Arrivals: Significantly down in Rajasthan due to farmer holding and earlier wheat arrivals disrupting auctions.

- Farmer Selling: Limited, as current prices do not meet expectations.

- Exports: Jan–Nov FY 2024–25: 54,830 tonnes (USD 6.89m), down from 100,334 tonnes (USD 10.46m) last year.

- Domestic Demand: Steady, but not strong enough to lift prices significantly.

📊 Fundamentals

- Sowing: Gujarat up slightly, Rajasthan and Madhya Pradesh down 25% due to adverse weather and low price realization.

- Stocks: Lower new crop arrivals, but old stocks are being held back by farmers.

- Speculative Positioning: Limited, with market participants expecting a narrow trading band.

⛅ Weather Outlook

- Rajasthan & Madhya Pradesh: Recent weather has been mostly dry, aiding harvest and storage, but last season's heavy rains and floods have left a mark on yield potential.

- Gujarat: Sowing conditions remain favorable, supporting a marginal increase in acreage.

- Short-term Outlook: No major weather disruptions expected in the coming week, supporting stable arrivals.

🌏 Global Production & Stock Comparison

💡 Trading Outlook & Recommendations

- Expect continued range-bound trading in the near term as arrivals and demand remain balanced.

- Monitor weather in Rajasthan and Gujarat for late-season risks.

- Exporters should remain cautious, as global demand is subdued and Indian FOB prices remain above some competitors.

- Buyers can consider gradual accumulation at current levels, as downside appears limited but upside is capped by weak exports.

- Watch for any policy changes or government procurement activity that could shift market sentiment.